Human

psychology is a powerful force and spoiler, especially in investing. We tend to

glorify our successes and ignore mistakes or best give it a passing reference

in coffee tables. Stock market investing is treacherous and requires strategy

and monitoring. Even if your strategy is subpar, a good monitoring system can

save the day. On the other hand, a great strategy with subpar monitoring can be

disastrous.

So

long as we earn money, we are savers and investors. Hence, it may be worthwhile

to recount some of the mistakes I have done while handling my savings,

especially in stock markets. Let us see what those mistakes are.

1.

Not having Endurance

Markets

are by nature volatile and hence make your emotions swing. It is normal to get

upbeat in a bull market (and laud your expertise) and disheartened in a bear

market (and curse bad time and luck). However, what is critical is your

endurance during the down market where your emotions are tested to the hilt. I

remember buying some of what is called today as blue chips way back in 1990’s

when I stepped into a career. If only I had the endurance to have held them

today, I could have retired a while ago! Instead, I gave into the market

psychology of selling when everyone was selling. Sometimes, your investments go

nowhere though they are not producing any losses. They can test your patience

since you will have the urge to compare them with broader market or with other

stocks. Stock price appreciation can never be a straight line. Many stocks have

a long time period of flat performance and then a takeoff (what I call as

inflection point). But the point is we cannot predict when that take off will happen.

Since we cannot predict this, we sometimes lose interest and exit the

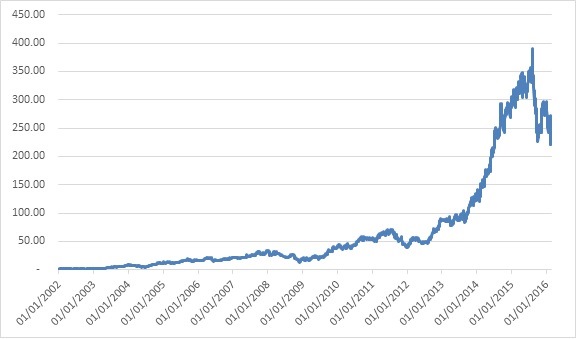

investment. That can prove costly as well. Here is an example of Eicher Motors.

Notice the long stretch of flat stock prices (2001 to 2009) hovering between

Rs.24 and Rs.400, and then a sudden burst of performance taking the stock price

all the way up to Rs.21,000 within a short span of time. If you were holding

this stock since 2001, it would have really tested your patience!

2.

Going by the Herd Mentality

Identifying

investment opportunities is a time consuming and lonely work. It requires

validation from several fronts including financial analysis, qualitative

analysis and connecting all the dots that are strewn all over the place. Even

then, one cannot be sure about the future prospects as on the date of

investing. However, there is an easy way of doing all this. Just go by what

your friends/colleagues/relatives are doing or what your brokers recommend. If

they are buying ITC, so buy it. If markets are going up, keep buying when the

trend is positive regardless of whether valuations are reasonable. This is a

sure recipe for underperformance. I used to compile the top holdings of all the

leading fund managers to see where they are investing in order to mimic their investments

only to realize that such a strategy is very similar to herd mentality which

the fund managers themselves are suffering from!

3.

Mistaking name/brand for profits

The

key indices (like Sensex and Nifty) are always dominated by large caps. By

definition, most of them would be market leaders in their respective industry

(Bajaj Auto, Infosys, Reliance, HDFC, ITC to name a few). Market leaders are

big brand owners. But being big and owning sexy brands do not equate to good

performance all the time. Sometimes, it is the small seemingly boring

businesses without any recognizable brand power that can create enormous

shareholder wealth, which is what we are concerned. Also, once a company

becomes large cap and brand leader, it may unnecessarily spend loads of money to

keep that status which can be a big negative for shareholders. No wonder, many

of the large caps in the index have poor performance track record during the

last 5/10 years in terms of creating shareholder wealth.

4.

Not acting when I should Have

It

is said that the easiest thing in the stock market is to buy and the toughest

is to sell. You will be forced to take a sell decision under three scenarios i.e.,

when you made good money and wondering if you want to take some profits, when

you have lost significantly and wondering if you should cut further losses or

when you have a liquidity need where you are forced to sell regardless of the

situation. The first is a good problem to have and the third is a bad problem

to have. However, the trickiest part is the second. This is where psychology

comes and acts as a spoiler. When your investment is down, your psyche refuses

to accept it as you feel you have grossly erred in your judgment. And also,

there is this innate feeling that this is temporary and the value will come

back. This feeling need not be backed by any logic. It can just be a feeling.

Also, you have a reference point i.e., your purchase price and your psychology

is swayed by this reference point. Unfortunately, the market does not know or

does not care what your reference point is. Hence, once the investment goes

down in value, it need not come back (as you innately feel). Rather it can go

down even further. I remember being caught in one such investment cycle where I

invested in a gulf stock called Gulf Finance House (GFH). Relative to my

investment value, my realized loss on that investment was 98%!. A classic

example of not acting when I should have.

5.

Averaging on the Downside

This

probably counts as a very common reaction when your investment value is down.

When the stock price tumbles, instead of fearing further downside our instincts

let us think that “if it was attractive at the earlier level when I bought, it

should be even more attractive now, so let me buy more”. Again the spoiler in

this situation is the reference point, which is your initial purchase price.

Your reference point has no reference value for the market and hence averaging

down on the downside can only result in “throwing good money after bad”. Since

markets are volatile, bounce backs are common and can make you feel that you

let a great opportunity to average your purchase price when the bounce back

happens. However, if price bounces back it will also make your investment look

good and hence should be of less worry. But if your averaging down does not pay

off, the net loss on that investment will be manifold. Hence, the need to wait

for the right price to buy stocks so that we are not caught in this dilemma of

“double down”! I am appending a table to illustrate this effect. During the

last one year, Nifty has been doing poorly so much so that out of 50 stocks in

Nifty 43 of them are in negative territory. All these 43 companies are ripe for

“averaging down” concept. The worst performer in Nifty during the last one year

was BHEL with a 61% fall in share price. The stock price plummeted from Rs.270

to about Rs.100 now. Any averaging along this path could have produced endless

pain. The same can be observed with other indices of NSE as well.

6.

Not being affected by loss on profits

Not

all losses are same. A loss of capital can produce more pain relative to say

loss in profits. Hence, complacency to deal with losses in the second case. We

panic the moment we have a loss of capital. But we do not show the same panic

when our profits are reduced though in

theory a loss is a loss. At least, that is how I dealt with my losses worrying

the most in cases where the capital is negative and not worrying about those

where it is a loss in profit situation. The best way to deal with this problem

is to equate your year-end market value to 100 and look at the appreciation/depreciation

from that perspective. Appended is a table with some hypothetical numbers to

explain the concept. If your investment starts at 100 and in a 5-year horizon

touches a peak of 150 and reverts back to 100, your compounded annual growth

rate (CAGR) will be 0 with no negative performance highlighted in the interim 5

years. Since you don’t see any negative performance, you may turn complacent to

loss in profits. However, if you equated the year end value to 100 every year,

years 3,4,and 5 would have highlighted negative performance. Such a performance

highlight could either have enabled you to take the profits or do something

else other than stare the stagnant performance.

7.

Not Insuring the portfolio

Insurance

need not be restricted to just life, cars and bikes. Even your stock portfolio

requires insurance lest you run the risk of swinging along with the market.

Like life insurance or other insurance products, portfolio insurance also will

cost you money. But that cost is bearable given the downside protection it

offers during sharp market downturns. Simple portfolio insurance example is to

buy put options. Fortunately Indian markets now offer such portfolio insurance

products. Even where you have investments only in mutual funds or ETF’s (for

some reason many think they are safe investments!), you still need to insure

your investment as your fund manager will not do it for you.

8.

Mistaking performance for stability

When

a stock performs well on the back of good company performance, we can mistake

it for stability and hence may fail to check the story at regular intervals.

Turning points, even in a good scenario, can be sudden and can wipe out gains

in no time. A recent example is Motherson Sumi, an auto ancillary company. Like

Eicher, the company had a long streak of ordinary performance and then had a

nice takeoff. From Rs.88 in Sept 2013, the stock went up to Rs.348 in August

2015. Not many paid attention to its over dependence on Volkswagen (40%) and

when bad news came in the form of scandal involving VW, the stock price of

Motherson Sumi plummeted 42% in just two months!

9.

Mistaking Performance for Skill

The

biggest mistake you can make as an investor is to attribute success to your

skill and failure to luck! (or bad luck!).

The performance of a company and therefore its stock price is dependent

on scores of quantitative and qualitative factors. While through skill you may

be able to crack the quantitative part, it is a time-consuming and innate exercise

to look through a company qualitatively. Qualitative factors include a deep

understanding of the Board and executive management, their track record in

terms of corporate governance, ethical conduct of the company and its owners, employee

remuneration, tweaking books to show a certain performance number, political

connections, front running the stock, insider trading, etc. Either you devote a

considerable time unlocking these essential elements to develop the needed

conviction or go with a gut feel on the subject. Given our inability to find

time, we normally resort to the second tactics. When your decision turns

positive, you feel you are in control of this process. Always double check the

story during a good performance period just to be sure you can keep the

profits.

Honestly

I have been through all these mistakes in one form or other. This list of

mistakes may not be exhaustive and I may unravel many more as I reflect.