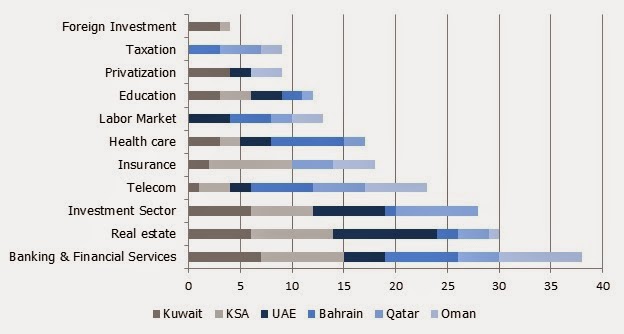

Over

the past three years, Kuwait has witnessed a raft of new regulations and

legislations aimed at making doing business in the country easier and

transparent. Some of the recent key legislations are recorded in the table

below –

Year

|

Legislative Authority

|

Brief Commentary

|

2010

|

Kuwaiti

Parliament

|

Privatization

law passed

|

2010

|

Kuwaiti

Government

|

Labor

Law for the private sector that details the procedures to be followed along

the full employment spectrum, right from recruitment to separation

|

2010

|

Central

Bank of Kuwait (CBK)

|

A

set of regulations was passed, in an effort to increase transparency,

accountability and overall health of the investment sector

|

2010

|

Kuwaiti

Parliament

|

Kuwait

Capital Markets Authority (CMA) comes into being

|

2012

|

CBK

|

CBK

issued new guidelines on governance at banks in Kuwait

|

2012

|

Kuwaiti

Government

|

Companies

Law passed in order to make doing business in Kuwait more attractive

|

2013

|

Kuwaiti

Parliament

|

A

law was approved to establish a SMEs fund, with a capital of KD2 billion (~$7

billion)

|

2013

|

CMA

|

Passed

a resolution on corporate governance rules applicable for listed companies

|

2013

|

Kuwaiti

Government

|

Anti-Corruption

Authority (ACA) established to tackle corruption in the handling of public

funds

|

2013

|

Kuwaiti

Government

|

A

new commercial licenses law completed that would reduce the bureaucracy

surrounding new businesses

|

2013

|

Kuwaiti

Government

|

The

maximum amount of home loans available to Kuwaiti women, increased, to KWD

70,000 from KWD 45,000, while the renovation amount that can be financed, has

been increased to KWD 35,000 from KWD 30,000

|

2013

|

Kuwaiti

Government

|

Law

No. 116 released promising a raft of FDI benefits, including 100% equity

ownership, 100% tax exemption for 10 years, partial/full tax exemption on

imports (raw materials, machinery & spare parts), land being made

available etc. The law was passed in order to promote FDI in Kuwait.

|

2013

|

Kuwaiti

Government

|

Kuwait

Direct Investment Promotion

Authority

(KDIPA) set up, as an enhanced successor of Kuwait Foreign Investment Bureau

(KFIB), for promotion of direct investment into Kuwait

|

2014

|

The

National Assembly

|

A

new Public Private Partnership (PPP) law that is essentially a modification

of the 2008 Build-Operate-Transfer (BOT) passed

|

2014

|

CBK

|

Foreign

banks allowed to open multiple branches in Kuwait

|

2014

|

CBK

|

Regulations

issued regarding Basel III Capital Adequacy Standard for banks

|

A

scan of the above list will tell us that the focus of Kuwait has been to

improve business governance within the country and strengthen regulations and

laws that would boost investor confidence. The 2009-2014 five year development

plan of Kuwait has seen only limited success, at best, with many of the

projects being transferred to the new five year plan of 2015-2020[1]. However,

despite the push ahead with multiple legislations and new bodies, there is

evidence that implementing change will not be easy. Media reports indicate that

the CMA is facing lot of pushback against its efforts to encourage corporate

information disclosure and in enforcing rules against excessively speculative

trading[2]. There

has been opposition to some of CMA policies that is causing delay in

implementation. For instance, the reforms deadline on the corporate governance

agenda has been pushed to June 2016[3].

The

case of Kuwait Airways is considered a good example of difficulties of

privatization in Kuwait. The Airline has been making losses for quite some time

and is taking steps such as retrenchment in order to cut down costs[4]. Yet,

privatization plans to modernize the airline and make it a more profitable

venture has elicited resistance from various stakeholders, including company

personnel and law makers[5]. Privatization

is expected to be a matter that would require great acumen and strategic

thinking in order to facilitate effective implementation across various

projects in the country. Closely linked to the theme of privatization is the

deeply felt need to making Kuwait a great place to do business, so that it can

effectively challenge regional and global leaders. In that regard, the relatively

new companies and licenses law are a great boost. However, these institutions

will need to be tied with larger reforms in education and infrastructure in

order for foreign companies and entities to feel enticed in order to benefit

from the tremendous business advantages that Kuwait offers.

On

the FDI front, the independent public authority, KDIPA, has complete control

over its own budget and recruitment process[6].

Kuwait’s Ministry of Finance presides over KDIPA, which among other factors, is

expected to streamline the process of decision making on FDI applications.

There is already some indication of this. In September 2014, Kuwait suspended

its offset obligations programme that compels foreign contractors, who win

sizeable government contracts in Kuwait, to invest in some prescribed fashion

in the Kuwaiti economy as part of a reciprocal gesture[7].

Even

as some broad ranging developments are taking place on the FDI front, there is

hope that Kuwait will see phased liberalization in the financial services

sector, as well, allowing the industry to match regional peers such as Dubai

and Doha . The decision of the CBK in March 2014 to allow multiple branches of

foreign banks, approved on a case by case basis, rather than only one country

branch allowed under the previous regulatory regime, should be seen in this

light[8].

Kuwait

passed an anti-corruption law in 2011, which included articles on money

laundering and financial disclosure[9]. In

June 2013, the anti-corruption body officially got its chief. Since then,

Kuwait’s anti-corruption authority has been steadily expanding its capacity

building and structural development activities[10].

Since the executive structures and administrative capacities of the authority

is in the process of solidification, it would be premature to pass an opinion

on the success of the body. However, the very fact that the body has been

officially created means that the government and the law makers are taking the

subject seriously, with more focus and effort expected in the years ahead in

what will, essentially, be a difficult and persistent exercise.

The

modification to the BOT law of 2008 means that local and foreign investors can

now avail of a project ownership duration of 50 years in comparison with the 40

years under the previous BOT rules[11]. This

is expected to encourage investments into mega projects due to the enhanced

incentive of an increased timeframe to reap the investment benefits. As Kuwait

attempts to develop a more favourable domestic energy mix in order to support

its larger oil revenues strategy, such regulatory developments are likely to

lend immense support. For instance, the Partnerships Technical Bureau (PTB) in

collaboration with Kuwait’s Ministry of Electricity and Water (MEW), are in the

process of developing an Integrated Solar Combined Cycle (ISCC) Plant to

generate power with a capacity of 280 MW[12]. The solar component will be 60 MW of the

total.

With

respect to the National Fund for Small and Medium Enterprises (SMEs)

Development, there is lot of promise in terms of the direction in which it is

moving. The KD 2 billion fund will not only provide finance for eligible

budding entrepreneurs, but will also offer support in terms of necessary

training courses[13].

Also, unlike previous small scale business funding experiments in Kuwait that

focused inordinately on low-risk projects, the new SMEs fund has the mandate to

cater to a calculated risk percentage, which is expected to encourage

entrepreneurs to innovate[14]. Regulatory

support in terms of the labour and companies law is expected to instill greater

confidence in the minds of aspirational entrepreneurs and the employees therein.

The

new institutions and legislations in Kuwait are trying to work in two

concurrent directions. While focusing on promoting the private sector and

foreign investors for economic diversification; there are also efforts at

boosting financial reforms, both in the private (e.g., banks) and the public

domain (government revenues and spending). It is encouraging to note Kuwait

buzzing with institutional building activities. This will surely form the

bedrock for further investments.

.jpg)